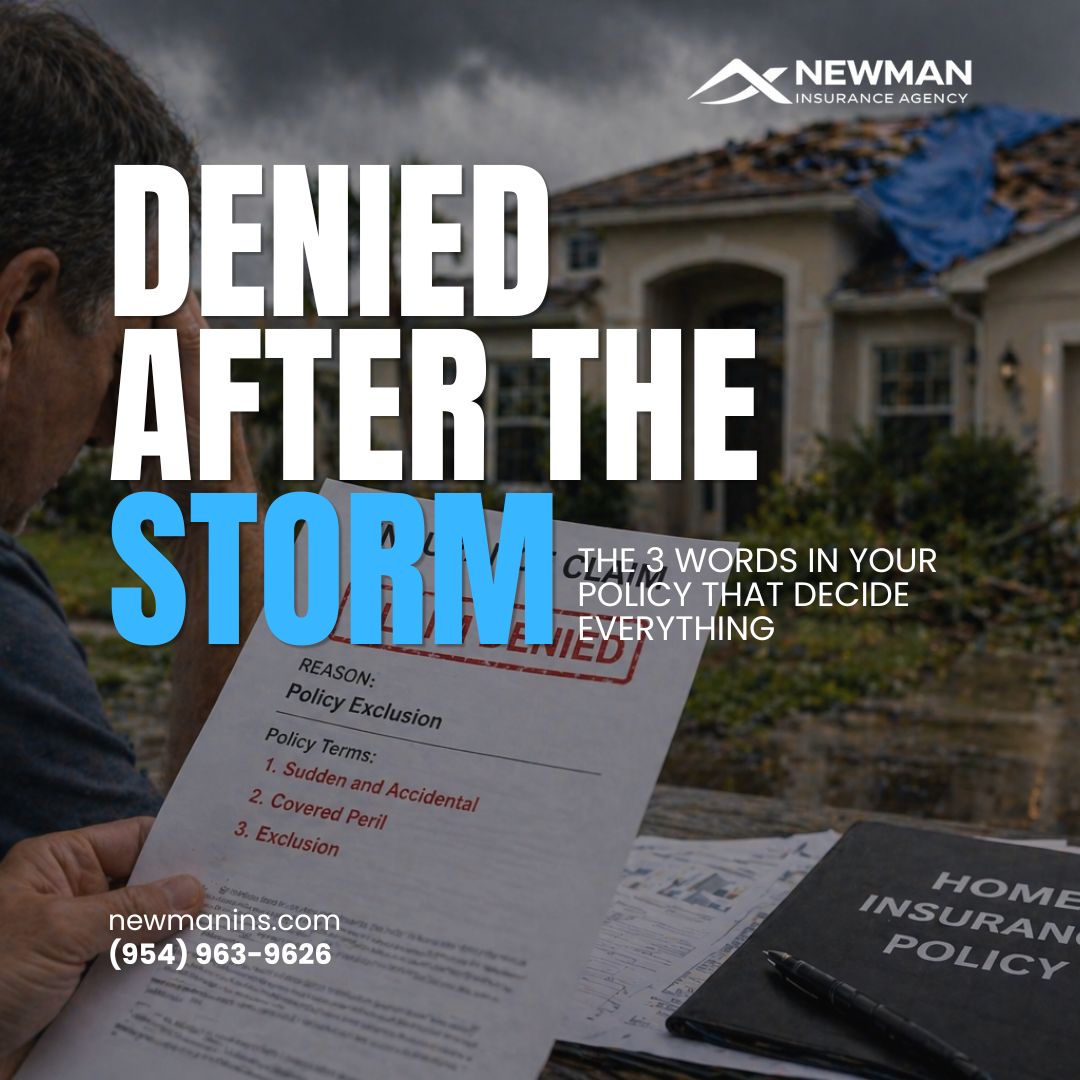

Your Roof Is Not Covered the Way You Think It Is Most homeowners believe roof coverage is straightforward. A storm hits, the roof is damaged, and insurance pays to replace it. That is not how roof claims are actually handled. How Roof Claims Really Work Roof claims are one of the most scrutinized areas in Florida insurance. The outcome rarely comes down to whether damage exists. It comes...