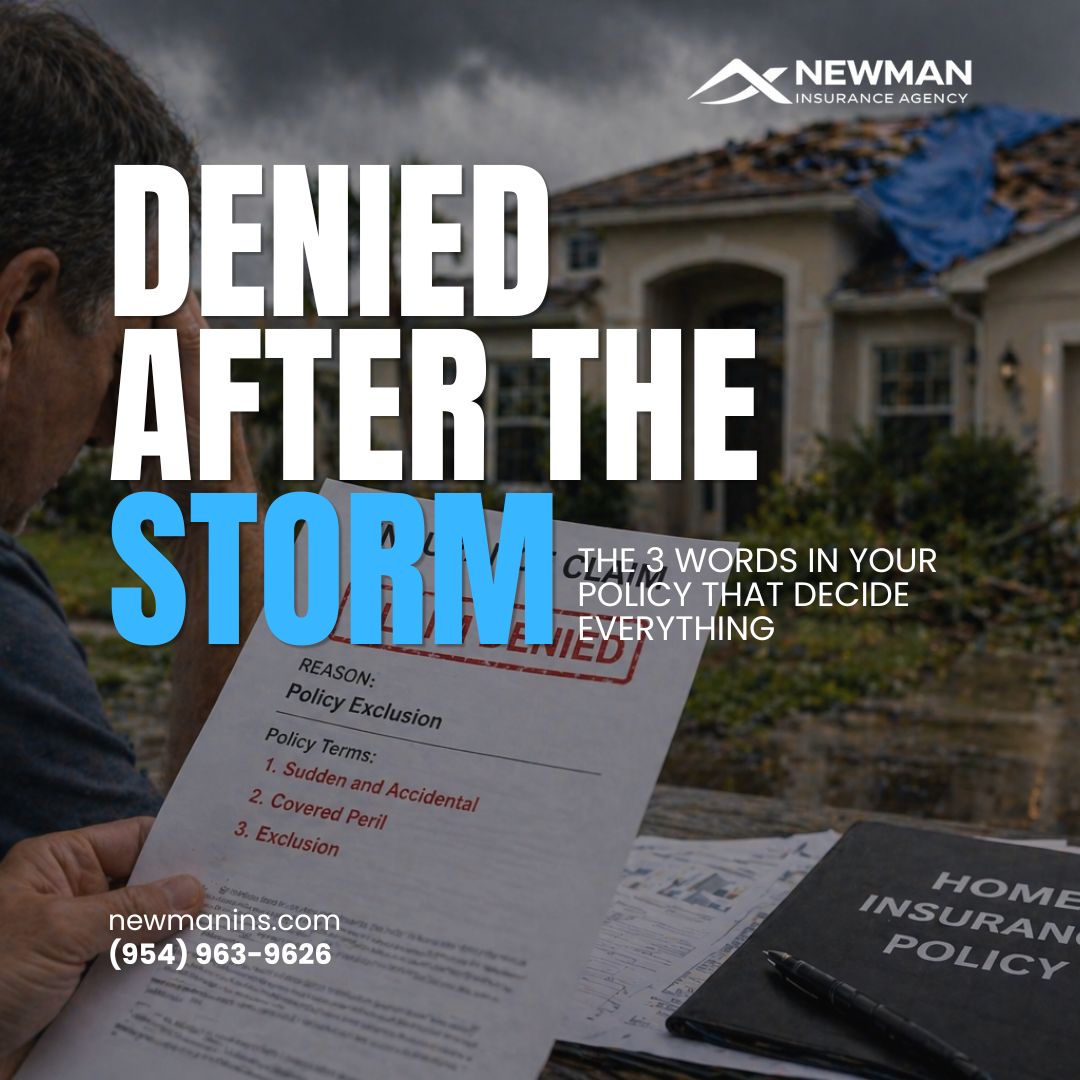

Denied After the Storm The Words in Your Policy That Decide Everything

After a major storm, most homeowners focus on the damage.

That is not what determines the outcome of a claim.

The deciding factor is the language inside your policy.

In many cases, a claim is approved or denied based on a few specific words that most people have never taken the time to understand.

The Phrase That Changes Everything

Most policies rely on the concept of sudden and accidental damage.

This means the loss must happen quickly and unexpectedly.

If an insurance company determines that the issue developed over time, even partially, the claim can be reduced or denied.

A roof that had prior wear or a leak that existed before the storm can shift the entire outcome.

What Counts as a Covered Cause

Not all policies cover the same types of events.

Some policies only respond to specific causes of loss.

If the cause is not listed, it is not covered.

Wind driven rain may be covered, while rising water is not.

To a homeowner, both feel like storm damage. To the policy, they are completely different events.

Where Most Claims Break Down

Exclusions define what is not covered, regardless of the situation.

Common examples include:

- Flood damage

- Mold beyond limited thresholds

- Wear and maintenance related issues

This is often where claims fail, even when the damage is severe.

Why Two Similar Homes Have Different Outcomes

It is not unusual for two homes in the same neighborhood to experience similar damage and have completely different claim results.

The difference is not the storm.

The difference is the policy.

What Homeowners Should Do

Review your policy language, not just your coverage limits.

Understand what triggers a claim and what prevents one.

Ask specifically about exclusions and how your coverage applies to different types of damage.

Bottom Line

Insurance is a contract.

And in that contract, wording matters more than anything else.

If you do not understand how your policy responds, you are relying on assumptions.

Those assumptions are often what lead to denied claims.

Know Before It Matters

Before the next storm, take the time to understand what your policy actually says.

It is the only way to avoid surprises when it matters most.